CBAM Quarter IV/2025 Reporting Period: Key Requirements to Be Completed Before 31/01/2026

From 2026 onward, the European Union (EU) will formally link carbon emissions to trade costs through the Carbon Border Adjustment Mechanism (CBAM). As a result, emissions data will no longer serve solely as an environmental reporting requirement. Instead, it will directly influence product pricing, customs clearance, and the overall competitiveness of exported goods.

In this context, the CBAM Quarter IV/2025 reporting period carries significance far beyond a routine compliance exercise. It represents the final dataset of the transitional phase and forms the foundation for the EU’s assessment of supply chain readiness before the official charging mechanism takes effect.

Enterprises that prepare thoroughly at this stage will be well positioned to manage risks and costs from 2026 onward. Conversely, gaps in data, processes, or traceability may translate into clear commercial disadvantages.

Key requirements to be completed before 31/01/2026

What Is CBAM and Why Must Businesses Engage?

The Carbon Border Adjustment Mechanism (CBAM) is an EU policy designed to align carbon costs between goods produced within the EU and imported products. Accordingly, imported goods are subject to an equivalent carbon price, calculated based on greenhouse gas emissions generated during their production.

Beyond reducing global emissions, CBAM aims to prevent “carbon leakage,” where production shifts to countries with lower environmental standards to reduce costs. In its initial phase, CBAM applies to high-emission sectors such as cement, iron and steel, aluminium, fertilizers, electricity, and hydrogen.

However, CBAM’s impact extends beyond directly regulated sectors. As the EU expands its scope and tightens data transparency requirements, indirect pressure increases across the entire supply chain. This includes raw materials, semi-finished products, and logistics.

Therefore, CBAM is evolving into a system-level compliance requirement for all businesses connected to the EU market.

CBAM (Carbon Border Adjustment Mechanism) of the EU

Why Is the CBAM Q4/2025 Reporting Period Decisive?

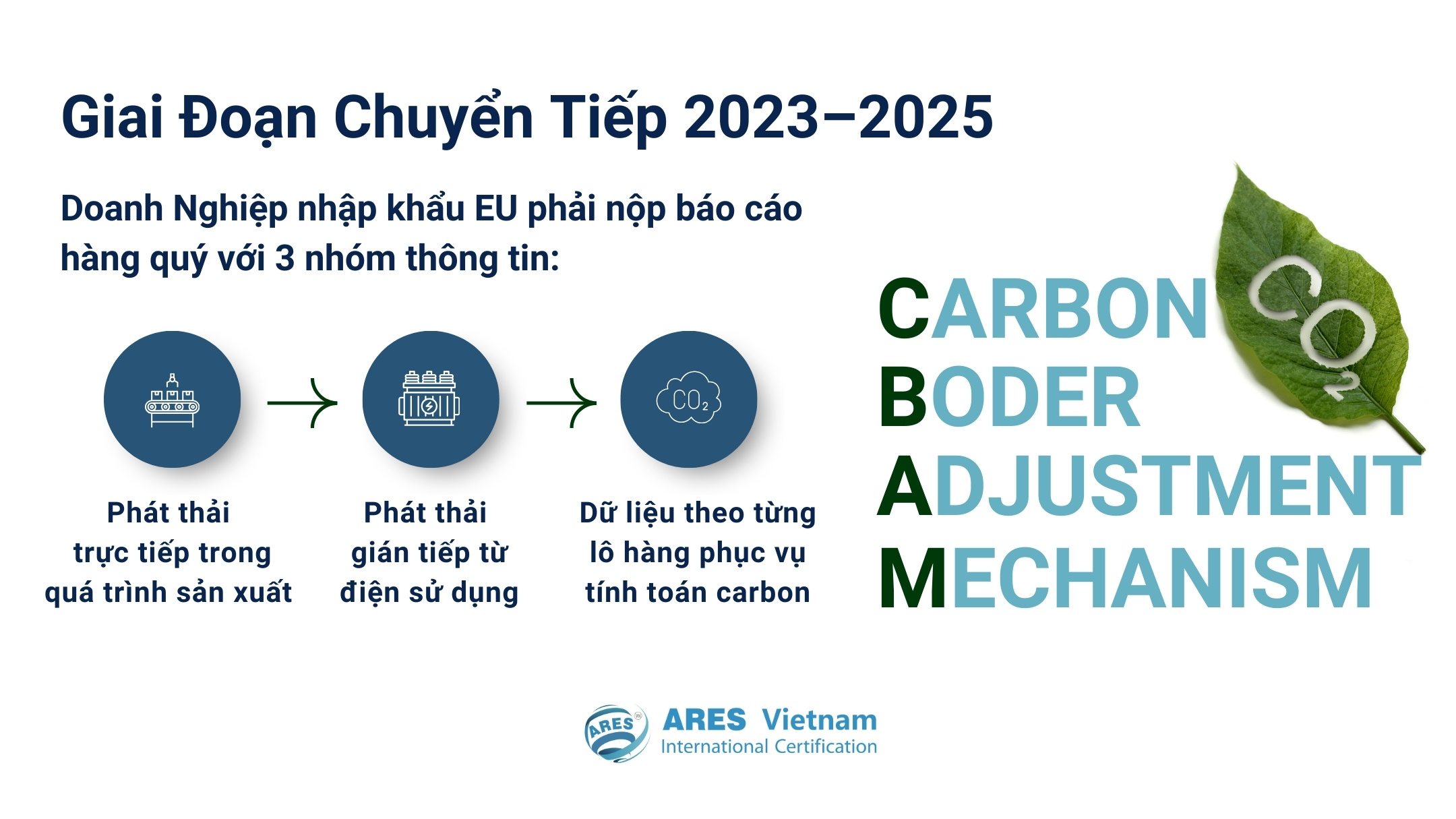

During the transitional phase from 1/10/2023 to 31/12/2025, CBAM has been implemented as a quarterly reporting obligation without financial charges. The primary objective is to help businesses familiarize themselves with EU-compliant emissions measurement, consolidation, and reporting.

Quarter IV/2025 marks the final reporting period of this phase. At the same time, it is the point at which the EU evaluates data stability, consistency, and verifiability before introducing carbon charges in 2026. The figures submitted during this period are considered key reference data, reflecting the maturity of carbon management systems at both enterprise and supply chain levels.

According to CBAM implementation analyses, the Quarter IV/2025 assessment focuses on three core dimensions:

◾Emissions data coverage: Whether all relevant CO₂ emission sources are fully identified within the defined scope.

◾Consistency across reporting periods: Whether calculation methods and data aggregation remain stable and aligned across quarters.

◾Traceability and verifiability: Whether emissions data can be traced to specific processes, batches, and emission sources.

From this perspective, CBAM is no longer merely a reporting obligation. Instead, it has become a benchmark for transparency and data governance capability in the EU market.

Key Information On The CBAM Quarter IV/2025 Reporting Period

According to guidance issued by the European Commission, importers and businesses must complete the following requirements during the CBAM Quarter IV/2025 reporting period:

◾Reporting period: October to December 2025

◾Reporting entities: Importers of CBAM-listed goods into the EU (cement, iron and steel, aluminium, fertilizers, electricity, hydrogen)

◾Reporting content:

- Detailed information on imported goods

- Greenhouse gas emissions data, classified by Scope 1, Scope 2, and Scope 3

- Actual emissions data or estimated values where direct measurement is not yet available

◾Submission deadline: 31/01/2026

Together, these requirements form the legal and technical foundation for CBAM’s charging phase. At the same time, they establish higher expectations for data standardization among exporting enterprises.

Key information on the CBAM Quarter IV/2025 reporting period

Potential Risks As CBAM Enters The Charging Phase In 2026

Once carbon emissions are directly converted into costs, even minor data discrepancies may lead to material financial and commercial consequences. Industry analyses, particularly in the steel sector and trade integration organizations, indicate that the greatest risk lies not in emission levels themselves, but in the ability to substantiate and defend reported data.

Where CBAM documentation lacks consistency, traceability by batch, or clear linkage across production stages, enterprises may face:

◾Adjustments or rejection of declared emissions data, resulting in higher CBAM costs than actual emissions.

◾Customs clearance delays, extended delivery timelines, and order disruptions.

◾Increased pressure from EU partners during price negotiations, especially for mid- and long-term contracts.

As CBAM increasingly becomes a market access condition, data weaknesses may lead to exclusion from preferred supply chains, even when production capacity and product quality remain unchanged.

Notably, these risks do not suddenly arise in 2026; rather, they are shaped during the Quarter IV/2025 reporting period.

Key Preparation Priorities 31/01/2026

By mid-January 2026, the remaining timeframe before the CBAM Quarter IV/2025 submission deadline is extremely limited. Therefore, the current priority is no longer long-term strategy development. Instead, it lies in completing mandatory elements that ensure report acceptance and minimize exposure during EU data verification.

Below are the actual values businesses need to prioritize to complete immediately:

1. Finalize Emissions Scope And Calculation Methodology For Quarter IV/2025

Enterprises should adopt a single, consistent calculation approach for the entire reporting period. Key actions include:

◾Clearly defining Scope 1 and Scope 2 emission sources applicable to EU-bound products.

◾Reviewing assumptions and emission factors to ensure alignment with CBAM guidance.

◾Delimiting Scope 3 data directly linked to the supply chain, at a level that can be reasonably explained.

At this stage, consistency and explainability are more critical than pursuing absolute precision.

2. Complete Emissions Datasets Linked To Each Shipment

CBAM assessments rely heavily on shipment-level traceability. Accordingly, enterprises should:

◾Link emissions data to each export order or shipment in Quarter IV/2025.

◾Verify consistency between production data, energy consumption, and export records.

◾Retain calculation sheets, templates, and source data for future clarification.

Where data exists only in aggregated form, the likelihood of adjustments or estimations increases significantly.

3. Align Supply Chain Documentation Directly Related To CBAM Products

Rather than attempting to cover the entire supply chain, enterprises should focus on key elements that directly impact reported products, including:

◾Core input material documentation.

◾Relevant transportation and logistics information.

◾Supplier-provided carbon data, where available.

The objective is to demonstrate continuous data flow, even if full Scope 3 coverage is not yet achievable.

4. Review Consistency Across Previous Reporting Periods

The Quarter IV/2025 report is assessed in comparison with earlier submissions. Companies should:

◾Compare emission levels, calculation methods, and data scopes across quarters.

◾Clearly explain significant fluctuations, where applicable.

◾Prepare justification for unavoidable changes.

Inconsistency between reporting periods remains one of the most common factors contributing to elevated CBAM risk assessments.

5. Prepare Supporting Documentation And Define Internal Responsibilities

As deadlines approach, CBAM becomes a matter of documentation governance, not only technical measurement. Companies should:

◾Assign clear responsibility for data consolidation and report submission.

◾Prepare explanatory documentation, including methodologies, assumptions, and data sources.

◾Ensure rapid response capability to clarification requests from importers or EU authorities.

Thorough preparation at this stage helps prevent reactive responses and reduces post-deadline pressure.

Key Preparation Priorities 31/01/2026

CBAM Q4/2025: Compliance Obligation Or Strategic Advantage?

The CBAM Quarter IV/2025 reporting period marks a critical transition, where emissions data directly determines access to the EU market. For enterprises that engage proactively, CBAM represents more than a legal requirement. It offers an opportunity to strengthen governance capacity, enhance transparency, and build long-term competitive advantage.

By standardizing emissions data, integrating CBAM into ISO management systems, and developing structured decarbonization strategies, businesses can not only manage carbon costs effectively, but also reinforce their sustainable position within global supply chains.

Explore comprehensive CBAM solutions and emissions management frameworks with ARES Vietnam.

Related news

ISO And Compliance Trends In 2026 That Vietnamese Businesses Should Not Overlook

Read more

Important Update for Food Businesses: From 2026, HACCP, ISO 22000, and FSSC 22000 Will Not Replace the Food Safety Eligibility Certificate

Read more

Looking Back at the Journey of 2025 – A Year of Value and Trust

Read more

International ISO Certification Standards

Read more

ARES Vietnam Awards ISO 9001:2015 Certification To Dong Nguyen Design Construction Co., Ltd.

Read more